Stamp Duty’s Crucial Influence on Cross-Border Capital Flows

Stamp duty plays a pivotal role as a fiscal mechanism shaping the movement of capital across international borders, particularly within active financial links such as the corridor connecting Hong Kong and Mainland China. More than a simple administrative fee, this tax directly impacts investment considerations, market ease of trading (liquidity), and the overall feasibility of transactions. Its application introduces costs and layers of complexity that require careful evaluation by investors and financial entities operating within these interconnected markets. A thorough understanding of its specific features and implications is therefore vital for effectively navigating the landscape of cross-border investment and capital deployment.

A primary effect of stamp duty in this context is its influence on the transaction costs borne by investors. Levied on specific transfers of assets, most notably real estate and securities, it represents a direct expenditure incurred during both buying and selling activities. For cross-border transactions between Hong Kong and Mainland China, investors must contend with two distinct duty systems, each possessing unique rates and triggering events. This direct financial cost diminishes the potential net return on investment, increasing the expense of executing transactions and potentially discouraging marginal investment opportunities. The impact is particularly significant in scenarios involving high-frequency trading or large-value transfers, where even seemingly minor percentage rates translate into substantial monetary outlays.

Furthermore, stamp duty significantly differentiates the financial viability of various investment strategies, notably distinguishing between short-term and long-term approaches. Strategies involving frequent asset turnover, such as day trading or rapid arbitrage, incur stamp duty costs repeatedly over short periods. This cumulative imposition can quickly erode potential profits, rendering such tactics less feasible or less profitable in jurisdictions with higher stamp duty burdens. Conversely, long-term investors who hold assets for extended durations encounter the duty less frequently, thereby reducing its relative impact on their overall returns. This dynamic encourages longer holding periods for cross-border capital, which can consequently influence market liquidity and the types of investment behaviors observed.

From a regulatory standpoint, stamp duty policies reflect each jurisdiction’s approach to taxing capital transfers. While both Hong Kong and Mainland China employ stamp duty, their specific frameworks—including rates, taxable bases, and exemptions—vary considerably. These differences not only affect costs but also highlight diverse policy objectives, ranging from generating government revenue and stabilizing markets to potentially discouraging speculative activity. The interaction and divergence between these distinct regulatory structures are critical factors for ensuring compliance and predicting the tax implications of cross-border transactions, underscoring stamp duty’s fundamental role in shaping the movement and allocation of capital.

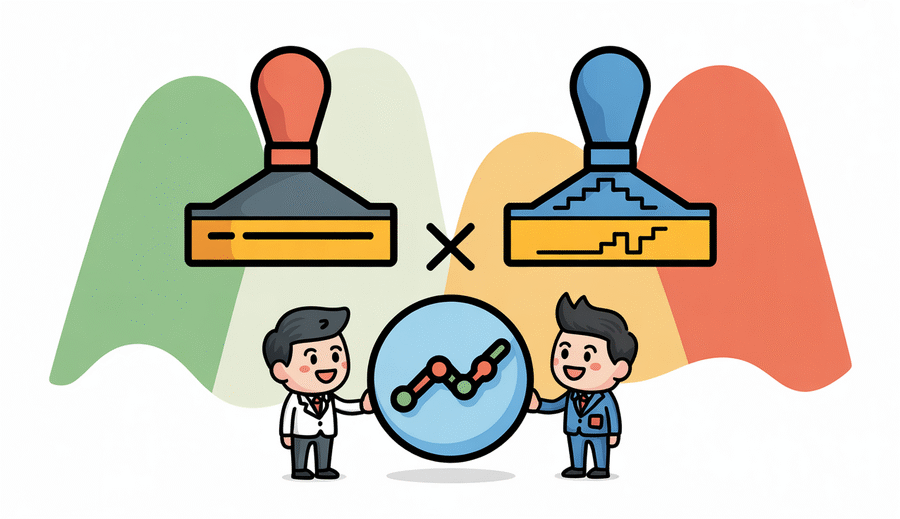

Structural Contrasts: Hong Kong’s Flat Rate vs. Mainland’s System

One of the most pronounced differences between the stamp duty regimes of Hong Kong and Mainland China lies in their foundational structures, particularly concerning transactions in equity markets. Hong Kong primarily employs a flat-rate system for stock transfers, offering investors a degree of predictability regarding transaction costs. In contrast, Mainland China’s approach, while subject to policy evolution, has historically shown capacity for variations in rate application and application method, differing from Hong Kong’s simpler, two-sided flat rate. Recognizing this core structural divergence is essential for any investor operating across these borders.

In Hong Kong, stamp duty on stock transfers is imposed at a fixed percentage rate, currently applied at 0.13% of the transaction value, payable by both the buyer and the seller (totaling 0.26%). This symmetrical, flat-rate application provides a consistent and easily calculable cost regardless of trade size or complexity, contributing to a clear cost structure within the Hong Kong equity market.

Mainland China’s system for stock trades, while simplified in recent years, has differed historically and in application. While previous structures may have included sliding scales or varied rates, the current prevalent practice applies a flat rate, often cited within a range such as 0.05%, but typically levied *only* on the seller side of the transaction. This differs fundamentally from Hong Kong’s model where both parties pay, impacting the net cost of trading equities and requiring investors to understand which party bears the duty.

Furthermore, the range of taxable events subject to stamp duty differs between the two jurisdictions. While both impose duties on equity and property transfers, the specific definitions, rates, and regulations for other documents or transactions can vary significantly. For example, Mainland China’s stamp duty extends to a broader spectrum of commercial documents and contracts beyond just equities and property, whereas Hong Kong’s application is generally more concentrated on these two primary asset classes. This difference in scope means investors operating in Mainland China must be aware of potential stamp duty implications on a wider variety of business activities.

The table below highlights key structural differences, focusing on common equity transactions and scope:

| Aspect | Hong Kong Stamp Duty (Equity) | Mainland China Stamp Duty (Equity & Scope) |

|---|---|---|

| Rate Structure (Equity) | Flat Rate System | Flat Rate System (but applied differently) |

| Typical Rate Range (Equity) | 0.13% (on each side, total 0.26%) | Around 0.05% (historically varied, currently typically flat) |

| Application on Equity | Paid by both Buyer and Seller | Typically paid only by Seller currently (Historically varied) |

| Primary Taxable Events Scope | Equity, Property | Equity, Property, various contracts & business documents |

These structural variations, encompassing rate methodology, application to parties, and the overall scope of covered transactions, significantly influence transaction costs and compliance requirements for investors conducting cross-border activities between Hong Kong and Mainland China. A detailed understanding of each jurisdiction’s specific rules is therefore critical.

Equity Market Impacts for Dual-Listed Companies

Dual-listed companies trading shares on both the Hong Kong and Mainland China equity markets encounter distinct implications directly arising from the different stamp duty regimes in each location. When investors trade shares of the same underlying company listed on different exchanges, such as H-shares in Hong Kong or A-shares in Shanghai or Shenzhen, they become subject to the respective local stamp duty rules. This difference is particularly relevant for participants using the Stock Connect programs, which facilitate cross-border equity trading. An investor buying an A-share via Stock Connect will incur the Mainland’s stamp duty (currently on the seller side), while a counterparty buying an H-share through the same mechanism will be subject to Hong Kong’s flat rate on both sides. This direct divergence in transaction cost significantly influences investor decisions, potentially biasing preference towards the market with the lower effective duty for specific trading strategies or asset classes, thus affecting cross-border capital flow dynamics.

The variation in stamp duty also has notable effects on the liquidity of the secondary market for these dual-listed securities. Transaction costs, including stamp duty, represent a fundamental friction to trading frequency and volume. Higher duty rates can discourage rapid trading and short-term positions, potentially leading to lower trading activity and reduced liquidity for certain share classes compared to their counterparts in the other market, even for the identical company. The H-shares market in Hong Kong and the A-shares market in Mainland China can consequently exhibit different liquidity profiles, partly attributable to the differing stamp duty burdens alongside other regulatory and market structure variances.

Furthermore, differential stamp duty rates are a crucial consideration for arbitrage strategies between H-shares and A-shares. As the shares of the same company can trade concurrently on the Hong Kong and Mainland exchanges, often presenting price disparities, arbitrage opportunities naturally emerge. However, capitalizing on these price differences requires executing trades in both markets, thereby incurring transaction costs at each step. Stamp duty constitutes a non-negligible cost component that arbitrageurs must meticulously factor into their calculations when assessing the profitability and feasibility of such cross-market strategies. The difference in stamp duty applicable to trading H-shares versus A-shares directly impacts the required price spread necessary for an arbitrage opportunity to be profitable after accounting for costs, influencing the extent to which prices converge or diverge and ultimately affecting the efficiency of the cross-border equity market link.

Analyzing Real Estate Investment Costs

Examining the cost structure for cross-border real estate investment between Hong Kong and Mainland China reveals significant differences in applicable stamp duties, a critical factor influencing transaction costs and investment feasibility. These duties vary not only in their percentage rates but also in how they are applied based on property type, buyer residency status, and the value of the transaction.

Generally, stamp duty rates on property transfers in Mainland China typically range from 3% to 5%, although specific rates can differ based on the property’s value, its classification (e.g., residential vs. non-residential), and local government regulations. Hong Kong, in contrast, applies an Ad Valorem Stamp Duty (AVD) scale for property transactions. For residential properties, this typically ranges from 1.5% to 4.25% based on a progressive scale tied to the transaction value. Commercial properties in Hong Kong have historically been subject to different duty rates than residential ones, further segmenting market costs.

A key divergence exists regarding special duties, particularly impacting non-resident buyers. Hong Kong previously implemented a Buyer’s Stamp Duty (BSD) specifically targeting non-permanent residents and corporate buyers, imposing a substantial additional cost on top of the standard AVD. While recent policy adjustments have significantly modified the treatment for non-permanent residents, the concept of differentiated duty based on residency has been a notable characteristic. Mainland China also imposes various taxes and fees related to property ownership and transfer that can affect foreign investors, though their structure and impact may differ from Hong Kong’s specific stamp duty mechanisms.

Moreover, the distinction between commercial and residential properties fundamentally impacts stamp duty calculations in both jurisdictions. Each category typically features a distinct rate structure or set of rules governing its transfer, meaning an investor’s choice of asset class—whether acquiring an office unit in Shanghai or a residential apartment in Kowloon—will directly determine the applicable stamp duty payable. Understanding these different scales and specific provisions is essential for accurately projecting total acquisition costs and evaluating the financial viability of cross-border real estate ventures.

Compliance Challenges for Cross-Border Transactions

Cross-border transactions involving Hong Kong and Mainland China, particularly those concerning assets subject to stamp duty like equities or real estate, introduce a substantial layer of compliance complexity for both investors and businesses. Navigating the distinct regulatory frameworks of two separate jurisdictions simultaneously creates unique operational and legal challenges. A primary difficulty is managing the dual-jurisdiction reporting obligations. Each territory possesses its own specific forms, filing deadlines, procedural nuances, and requirements for supporting documentation when declaring transactions and paying applicable stamp duty. What satisfies the Hong Kong Inland Revenue Department may not be sufficient or in the correct format for the tax authorities in Mainland China, demanding meticulous attention to detail. This duality necessitates understanding differing legal interpretations, administrative practices, and often involves overcoming language barriers, requiring adherence to separate sets of rules and submission protocols for the same underlying transaction.

Furthermore, both Hong Kong and Mainland China maintain sophisticated measures aimed at preventing tax avoidance, specifically designed to deter individuals and entities from structuring transactions solely to evade or minimize stamp duty liabilities. These measures can include scrutinizing the economic substance of a transaction over its legal form, challenging asset valuations used for duty calculation, or recharacterizing complex arrangements deemed artificial. Ensuring compliance involves not only correctly calculating and paying the applicable duty based on explicit rules but also structuring transactions and valuations in a manner that can withstand potential review and challenge by tax authorities in one or both jurisdictions. Understanding the specific anti-avoidance provisions relevant to cross-border capital or asset movements, including those targeting related-party transfers or indirect disposals, is crucial for mitigating compliance risk effectively.

Finally, establishing and maintaining robust documentation standards is paramount for creating clear and defensible audit trails. Tax authorities in both Hong Kong and the Mainland may require extensive documentation to verify the nature of a transaction, the valuation of assets, the identities of participating parties, and the accuracy of stamp duty calculations. This typically includes original sale and purchase agreements, independent valuation reports where relevant, evidence of payment, records detailing previous transfers or holding periods, and necessary corporate approvals like board resolutions. The level of detail, the required format for submission (whether physical or electronic), and the mandated retention periods for such documentation can differ between jurisdictions, adding another layer of administrative complexity. Proper, verifiable record-keeping is essential not only for initial filing but also for successfully managing any subsequent inquiries, audits, or investigations from either tax jurisdiction, highlighting the intricate compliance landscape inherent in cross-border Hong Kong-Mainland transactions and emphasizing the value of seeking professional guidance.

Strategic Approaches to Tax Mitigation

Navigating the distinct stamp duty landscapes of Hong Kong and Mainland China necessitates proactive strategies aimed at mitigating tax liabilities and optimizing investment returns. Investors face inherent complexities related to transactional costs and compliance, making careful planning indispensable. While stamp duty is a direct cost, approaches centered on structuring, timing, and leveraging international agreements can significantly enhance the tax efficiency of cross-border capital flows and asset transfers between these two jurisdictions. These methods collectively aim to minimize the overall tax burden associated with operating and investing across the border.

One fundamental mitigation strategy involves considered entity structuring. Utilizing a Hong Kong holding company is a widely adopted method for facilitating investments into Mainland China. Hong Kong’s favorable tax system, particularly its territorial basis of taxation, offers inherent advantages. Establishing an HK entity as an intermediary can streamline fund management and intercompany transactions. Such a structure is often instrumental in optimizing tax outcomes and frequently key to effectively accessing benefits provided by the Double Taxation Arrangement (DTA) between Mainland China and Hong Kong, offering flexibility in managing various income streams.

Tactical transaction timing presents another avenue for optimization. The tax regimes of both Hong Kong and Mainland China, including stamp duty rules, are subject to potential adjustments driven by economic conditions or government policy changes. Astute investors closely monitor proposed legislative or regulatory shifts. Strategically timing significant asset acquisitions or disposals, major capital movements, or corporate restructuring activities to coincide with periods offering the most favorable tax treatment can lead to considerable savings. This requires staying informed about the evolving regulatory environment and positioning transactions strategically before potential changes take effect.

Leveraging the Double Taxation Arrangement (DTA) between Mainland China and Hong Kong is critically important. This comprehensive agreement is designed to prevent cross-border investors from being subjected to double taxation on the same income or gains. While the DTA may not directly eliminate stamp duty itself, it significantly impacts related taxes on income streams such as dividends, interest, and potentially capital gains. Applying the specific provisions of the DTA allows eligible investors to potentially claim tax relief through mechanisms like tax credits, exemptions, or reduced withholding rates. Effective utilization requires careful planning and strict adherence to eligibility criteria and reporting requirements, thereby reducing the overall tax impact on cross-border investment returns.

Emerging Trends in Cross-Border Fiscal Policy

The fiscal environment governing interactions between Hong Kong and Mainland China is dynamic and continuously evolving. Investors and businesses must remain attentive to emerging trends that have the potential to reshape the landscape for cross-border capital flows and their associated tax burdens, including stamp duty. Several key areas indicate potential shifts in policy direction, reflecting both global developments and ongoing regional integration efforts. Understanding these evolving dynamics is crucial for effective strategic planning and compliance management.

One significant area of development concerns the taxation of digital assets. As cryptocurrencies, NFTs, and other forms of digital value gain traction, tax authorities globally are grappling with how to categorize and tax transactions involving them. While stamp duty traditionally applies to physical instruments and property, the principles established for taxing digital assets in both jurisdictions could set precedents for how future digital transactions are treated, potentially introducing new forms of transaction-based taxes or influencing asset valuations relevant to existing tax frameworks. Policies in this domain are developing rapidly and warrant close monitoring for their implications on cross-border financial activities.

Furthermore, ongoing integration efforts within the Greater Bay Area (GBA) present a unique context for fiscal policy evolution. Proposals frequently include measures aimed at facilitating the seamless flow of capital, talent, and goods within the region. While a full harmonization of tax systems is unlikely in the near term, specific GBA initiatives could lead to targeted tax relief, simplified procedures, or even pilot programs that alter the tax treatment of certain cross-border activities or investments originating from or directed into GBA cities. These regional policies may introduce nuances to the existing stamp duty structures and other fiscal rules governing cross-border investment specifically within the Greater Bay Area.

On a global scale, the implementation roadmaps for BEPS 2.0 (Base Erosion and Profit Shifting) initiatives, particularly related to Pillar One (Addressing the Tax Challenges Arising from the Digitalisation of the Economy) and Pillar Two (Global Anti-Base Erosion Rules), are compelling jurisdictions worldwide, including Hong Kong and Mainland China, to adapt their corporate tax frameworks. While BEPS 2.0 primarily targets large multinational enterprises and focuses on corporate income tax rather than directly impacting stamp duty, the resulting changes in tax structures and compliance requirements can significantly influence corporate investment decisions, entity structuring choices, and the perceived attractiveness of different locations for holding assets. This broader shift in international taxation indirectly affects the context within which cross-border investment between the two regions operates and contributes to the overall tax burden faced by multinational businesses. Navigating this confluence of global and regional fiscal shifts requires proactive engagement with tax advisors knowledgeable in the intricacies of both jurisdictions.