Understanding Stamp Duty Fundamentals in Key Financial Hubs

Stamp duty is a fundamental fiscal instrument used by governments in major financial centers such as Hong Kong, Singapore, and London. This tax is primarily levied on specific legal documents and transactions, serving both as a significant source of government revenue and a mechanism for formalizing agreements. In Hong Kong, stamp duty notably applies to property transactions and the transfer of shares. Whether involving residential or commercial real estate, or trading securities listed on the stock exchange, understanding stamp duty is essential for market participants.

Comparing the core tax structures across Singapore and London reveals shared principles but distinct implementations. Singapore, like Hong Kong, imposes stamp duty on documents related to immovable property and stocks and shares. However, the specific definitions of taxable documents and the associated administrative procedures can differ. London, representing the United Kingdom, operates its own stamp duty system, including Stamp Duty Land Tax (SDLT) for property transactions and Stamp Duty or Stamp Duty Reserve Tax (SDRT) for share transfers. While these three hubs target similar asset classes, the precise scope, thresholds, and historical evolution of their respective duties reflect unique legislative histories and economic priorities.

The primary objective behind collecting stamp duty in these jurisdictions is consistently revenue generation for the state. Governments rely on these taxes on high-value transactions to contribute substantially to public finances. Beyond revenue, stamp duty can also serve policy goals, such as potentially influencing market behavior by discouraging property speculation or managing trading volumes. It also plays a vital role in formally recording and validating certain legal transactions, providing a clear audit trail for changes in ownership. While revenue remains paramount, the specific design and application of stamp duty in Hong Kong, Singapore, and London are shaped by each jurisdiction’s broader economic strategy and tax policy objectives.

Side-by-Side Rate Comparison for Equity Transactions

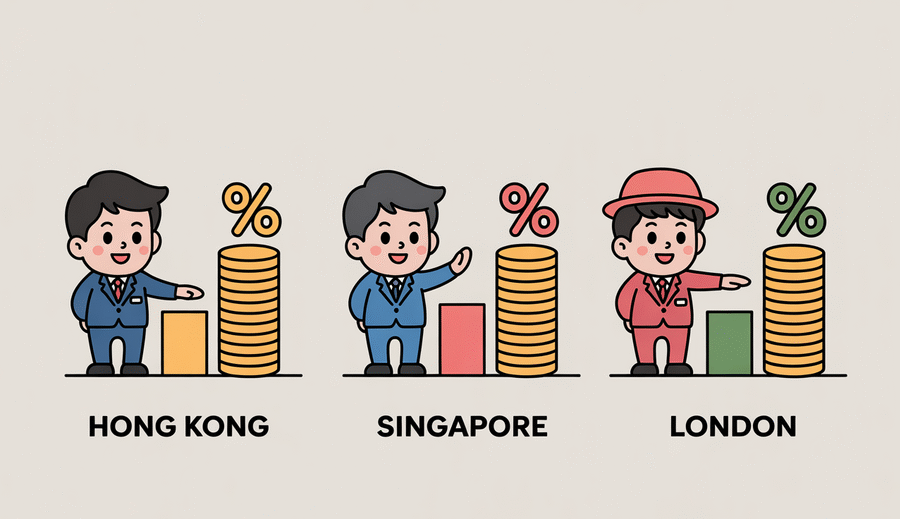

Examining Hong Kong’s stamp duty on equity transactions provides a clear benchmark for comparing trading costs across major financial hubs. For shares listed on the Stock Exchange of Hong Kong, duty is applied to both the buyer and the seller upon transfer. The current rate for this share transfer duty is 0.1% of the consideration or market value of the shares, whichever is higher, levied on each party. This results in a total effective duty of 0.2% on the transaction value, split equally between the buyer and the seller. This fixed, double-sided percentage establishes a clear and predictable cost structure for equity transactions in Hong Kong.

Singapore’s system for listed shares differs by typically levying stamp duty solely on the buyer. The standard rate is 0.2% of the consideration paid for the shares. This single-sided imposition at a fixed rate contrasts with Hong Kong’s approach. While other asset classes or historical rules might involve tiered systems, for contemporary listed share transactions, the 0.2% rate borne by the buyer is the primary point of comparison in this context.

London’s stamp duty regime for UK-listed shares involves Stamp Duty or Stamp Duty Reserve Tax (SDRT), generally applied at a rate of 0.5% of the consideration. Similar to Singapore, this duty is typically paid by the buyer. A key distinction compared to both Hong Kong and Singapore is the potential for exemptions within the UK system, particularly for transactions executed on certain overseas exchanges or through specific clearing systems. These exemptions can offer cost advantages for international investors trading UK securities outside the standard London market mechanisms, adding a layer of complexity beyond the headline rate.

Analyzing these rates and structures side-by-side illustrates the differing transaction costs investors encounter across these hubs. The table below summarizes these key differences in how costs are applied to equity trading:

| Hub | Standard Rate (on value/consideration) | Payer(s) | Key Feature |

|---|---|---|---|

| Hong Kong | 0.1% (total 0.2%) | Buyer & Seller | Fixed rate, double-sided |

| Singapore | 0.2% | Buyer | Fixed rate, single-sided |

| London (UK) | 0.5% | Buyer | Potential offshore exemptions |

The variance in duty rates and their application—whether fixed, potentially subject to exemption, and paid by buyer, seller, or both—significantly influences the overall transaction cost of trading equities. These distinctions are material factors affecting trading strategies, market liquidity, and the relative appeal of each financial center for different types of equity trading activities, especially for high-frequency or large-volume participants where marginal costs can accumulate rapidly.

Impact on Market Liquidity and Trading Volumes

Transaction costs, such as stamp duty, significantly influence the overall liquidity and trading volumes within a financial market. Understanding this impact is crucial for assessing the health and competitiveness of major financial hubs. Higher transaction costs can act as a direct deterrent to trading activity, potentially slowing down the velocity of capital within the market.

A clear correlation is often observed between stamp duty rates and stock market turnover trends. When the cost of buying and selling shares increases due to duties, investors and traders may become less inclined to engage in frequent transactions. This can lead to reduced trading volumes and potentially lower market liquidity, making it harder for participants to enter or exit positions efficiently without significantly impacting prices.

The impact extends particularly to smaller entities. The burden of stamp duty can disproportionately affect the attractiveness of listing for small and medium-sized enterprises (SMEs) in high-tax jurisdictions. Reduced liquidity stemming from higher trading costs can make shares less appealing to investors, which in turn might deter SMEs from seeking public listing or could hinder their ability to raise follow-on capital through the market.

Furthermore, sophisticated trading strategies, including algorithmic and high-frequency trading, are acutely sensitive to transaction costs. Even marginal increases in stamp duty can erode the profitability of these strategies, which often rely on thin margins across numerous trades. Analysis following reforms in markets with changes to stamp duty has frequently shown quantifiable reductions in algorithmic trading volumes, underscoring their sensitivity to these specific costs. The following table summarizes some potential impacts:

| Market Aspect | Impact with Higher Stamp Duty | Impact with Lower Stamp Duty |

|---|---|---|

| Market Turnover | Typically reduced | Typically increased |

| SME Listing Attractiveness | Potentially diminished | Potentially enhanced |

| Algorithmic Trading Volume | Often significantly decreased | Often encouraged |

Ultimately, the design and level of stamp duty have tangible effects on the operational dynamics of a stock market, influencing daily trading volumes, the viability of advanced trading techniques, and the appeal for companies seeking to list.

Investor Behavior Across Tax Regimes

Tax policies, particularly transactional taxes like stamp duty, considerably influence how investors allocate capital and execute trades across different financial hubs. The variance in these levies among jurisdictions such as Hong Kong, Singapore, and London prompts distinct behavioral responses as market participants seek to optimize returns and minimize costs. Understanding these patterns is crucial for grasping the competitive dynamics of global financial centers.

One notable behavioral impact is the potential shift of capital towards markets or instruments with lower tax burdens. When equity transactions face significant stamp duty, investors may increasingly turn to alternative asset classes or derivatives markets. These markets often feature different, sometimes lower or even zero, transaction costs, providing a potential tax arbitrage opportunity. Tracking the flow of investment into derivatives compared to direct equity purchases can indicate the extent to which stamp duty influences this strategic allocation decision.

Furthermore, the specific structure of a tax regime can affect the adoption of particular investment vehicles. For instance, the tax framework in a hub like Singapore can influence the attractiveness and utilization of Special Purpose Acquisition Companies (SPACs). How stamp duty and other related taxes are applied to the formation, de-SPAC process, and trading of these vehicles can significantly impact investor appetite and the prevalence of SPAC listings compared to traditional IPOs in that market.

Cross-border investment patterns and corporate listing choices are also shaped by tax considerations. Stamp duty differentials between financial centers can play a role in decisions regarding dual listings, where a company lists its shares on exchanges in multiple jurisdictions. Investors holding shares in dual-listed companies might also choose to trade on the exchange with the lower stamp duty rate, if feasible, to reduce transaction costs. Mapping these cross-border trading and listing patterns helps illustrate the tangible impact of varying tax regimes on global market activity and investor strategy.

Recent Reforms and Competitive Adjustments

The landscape of stamp duty in major financial hubs is not static; it is subject to ongoing reform driven by competitive pressures and economic objectives. Recent years have seen notable adjustments aimed at fine-tuning these fiscal tools and enhancing market appeal. Hong Kong, for instance, implemented a significant change in late 2023, reducing the stamp duty rate on stock transactions from 0.13% to 0.1% for both buyers and sellers. This move was explicitly aimed at revitalizing market activity and boosting liquidity, responding to concerns about the duty’s impact on trading volumes and competitiveness compared to rival centers. Evaluating this reduction involves assessing its initial impact on turnover and investor sentiment, recognizing it as a strategic policy lever in the global competition for capital.

Singapore has also seen adjustments, particularly concerning its property stamp duties, which feature a progressive structure. Changes often involve recalibrating Additional Buyer’s Stamp Duty (ABSD) rates, especially for foreign buyers and entities, to manage housing demand and maintain affordability. While primarily focused on property rather than direct financial market transactions like share trading duty, these adjustments reflect a broader governmental approach to using taxation to influence specific economic behaviors and outcomes within its competitive framework. Comparing these changes highlights different jurisdictional priorities—Hong Kong focusing on capital market activity, Singapore often emphasizing property market stability and social objectives via ABSD.

Meanwhile, London’s post-Brexit environment has prompted a reassessment of its tax competitiveness, including stamp duty on share transactions (Stamp Duty Reserve Tax – SDRT) which stands at 0.5%. While this rate is currently higher than Hong Kong’s reduced rate, London benefits from certain exemptions and established market infrastructure. Assessing London’s position involves considering whether its current tax structure, alongside its regulatory environment and market depth, remains sufficiently attractive to international businesses and investors in a world where competing hubs are actively making adjustments to their own tax regimes. The pressure to maintain or enhance competitive advantage is a constant driver behind these varied reform efforts across Hong Kong, Singapore, and London.

Future Projections for Cross-Border Tax Policy

Looking ahead, the tax policies governing financial transactions in major hubs like Hong Kong, Singapore, and London are poised for further evolution. These jurisdictions constantly assess their regulatory frameworks to maintain competitiveness and adapt to changing global economic conditions and technological advancements. Predicting the precise trajectory is complex, but key trends point towards potential shifts driven by domestic pressures, technological integration, and international cooperation or competition.

For Hong Kong, the discussion around stamp duty, particularly on stock transactions, remains dynamic. Following recent adjustments, there is ongoing debate regarding the possibility of further reductions or even complete elimination in the long term. Such a move would likely be aimed at boosting market liquidity and attracting more capital, potentially aligning Hong Kong more closely with financial centers that impose minimal or no transaction taxes on equities. The timeline for such a significant change would depend on various factors, including government revenue needs, market performance, and competitive pressures from rival hubs.

Technological innovation is also expected to play a significant role in shaping future tax compliance and transaction processing. The increasing adoption of blockchain and distributed ledger technology could potentially revolutionize how cross-border transactions are recorded and taxed. These technologies offer the promise of enhanced transparency, automation, and efficiency in reporting and collecting duties, potentially reducing administrative burdens and minimizing evasion. Integrating such systems into existing tax frameworks across multiple jurisdictions presents a complex but potentially transformative opportunity.

Furthermore, financial hubs face increasing pressure to align their tax policies with broader international initiatives, such as global efforts towards enhanced tax transparency standards or considerations around digital taxation. While stamp duty is distinct from corporate income tax, the overall tax posture of a jurisdiction is under scrutiny. These global alignment pressures can influence how jurisdictions structure their tax incentives and collection methods to remain attractive while adhering to evolving international norms and agreements. The future landscape will likely be a blend of targeted duty adjustments, technological adoption, and strategic responses to global tax policy dialogues.